When discussing cryptocurrency, the question of use cases often arises. Sometimes, this question is used skeptically to dismiss projects before they gain traction, but it's also a valid inquiry that gets to the core of "why crypto?" What specific purpose does this particular coin or blockchain serve?

For Bitcoin, the often-cited use case is "store of value," meaning the coin itself holds value and, in theory, retains it or even appreciates against inflation. Another commonly mentioned use case for Ethereum and other cryptocurrencies is "banking the unbanked." This sounds promising, but what does it actually mean?

The Why:

Let's rewind to when crypto gained more mainstream attention in 2011. This period coincided with the Occupy Wall Street movement, and highlighted the inherent flaws in the modern financial system, prompting the search for alternative solutions. These solutions eventually evolved into crypto as we know it today, enabling borderless transactions and transcending systems perceived as rigged against ordinary people.

Fast forward to 2024. Empowering individuals remains the core concept of crypto. But how does this translate into "banking the unbanked"?

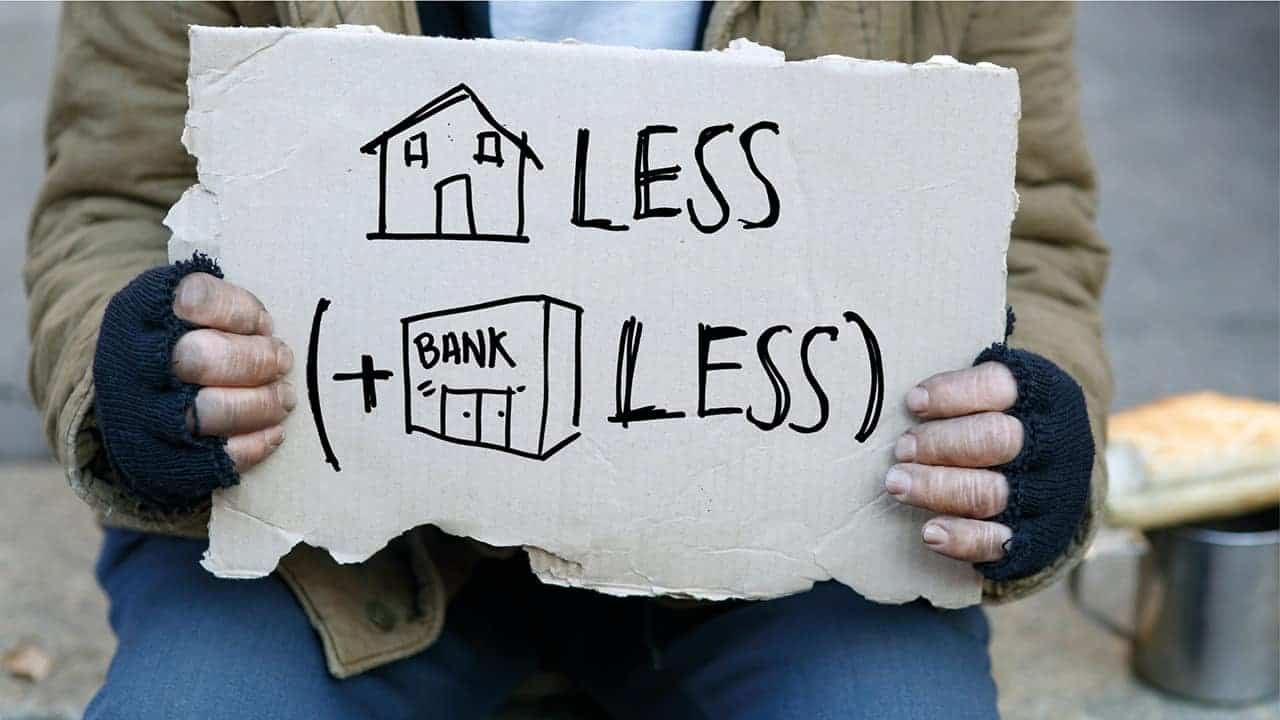

For those reading who have never been able to get a bank account, or had an account vaporized through bank insolvency, you understand the challenges. For others, consider a concrete example: Chase Bank in the United States.

Opening a Chase bank account is free, but the free part ends quickly. Maintaining a free account requires:

- $50,000 in invested assets or

- Over $2,000 combined in checking/savings accounts

If neither condition is met, Chase charges $15 per month. This policy disproportionately burdens low-income individuals, essentially penalizing the poorest by making them poorer.

In today's world, a bank account is crucial for essential tasks like paying bills, qualifying for loans, saving money, and protecting assets. Yet, according to World Bank data, over 1.4 billion adults remain unbanked, with even more underbanked (facing fees and limited access). This disproportionately affects the poor, uneducated, and women.

Banking the unbanked aims to empower this massive population with digital technologies and currencies.

The What:

This is where crypto offers a solution. With a crypto wallet, individuals gain complete ownership of their assets, free of charge. They can send and receive crypto, earn rewards, and spend it without restrictions. Best of all, good crypto wallets cost users nothing.

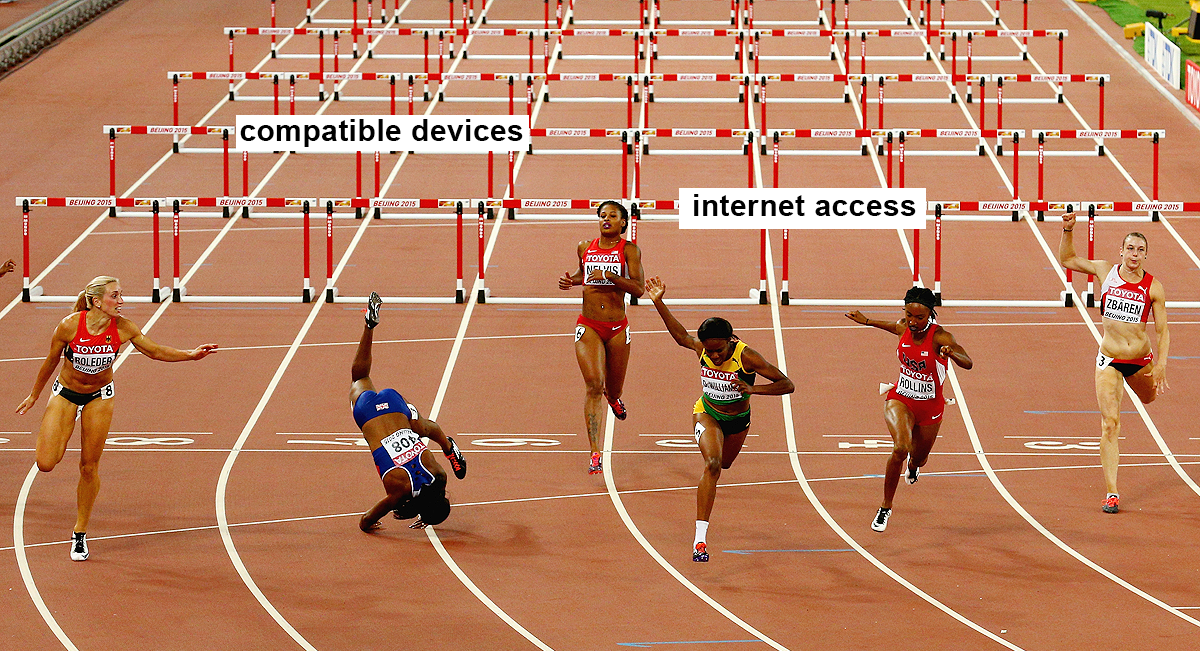

While internet access and a compatible device remain barriers, they are less insurmountable than traditional hurdles.

The How:

So, what are the essential features of a crypto wallet for banking the unbanked?

1. Self-custody: No third-party, company or otherwise should have access to the account or wallet. This fosters true ownership and prevents restrictions or unnecessary fees. While user responsibility increases, it's crucial for empowerment.

2. Open-source: The wallet application's technology should be verifiable, allowing any and all to look at the code and make sure everything is above board. This allows users to transfer their wallet safely using their recovery phrase, ensuring continued access even if the provider discontinues their service. This, in essence, speaks to number 1, proving to everyone that the wallet is self-custody.

3. User-friendliness: To onboard more people, the wallet needs to be simple to understand and use for daily tasks.

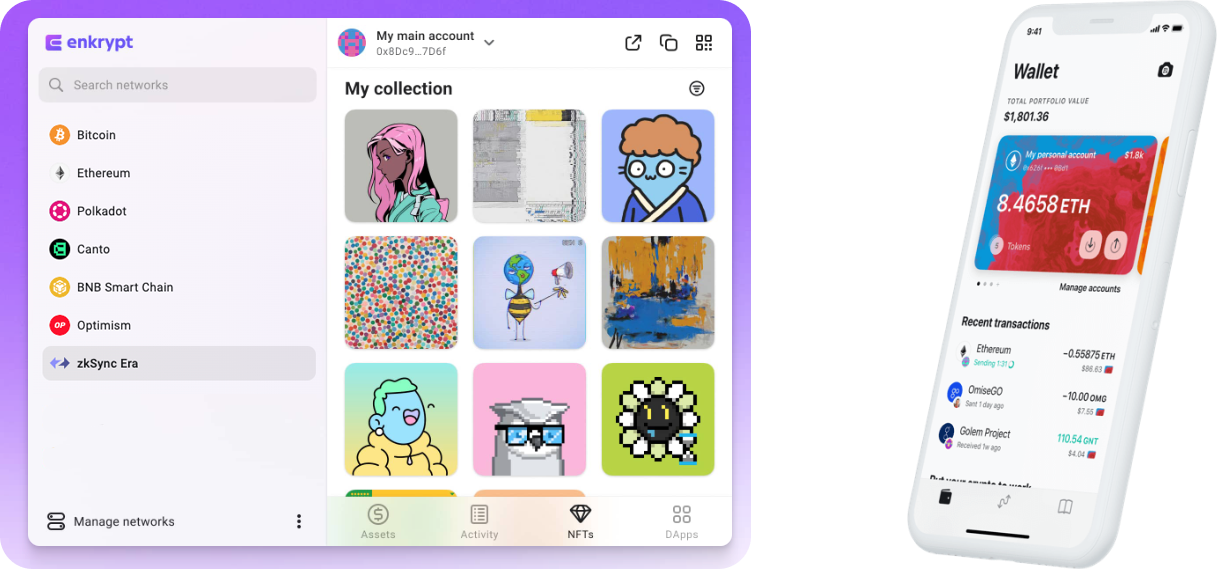

Fortunately, wallets like Enkrypt (browser) and MEW (mobile) fulfill these criteria.

So, next time someone asks about "banking the unbanked," consider showing them a self-custody wallet. This is how we can empower millions with crypto.

Thank you for checking out our article on Banking the Unbanked! Make sure to follow us on X(Twitter) and let us know your thoughts. Sign up for our newsletter to stay up to date with MEW releases, and check out our weekly podcast Crypto Currents for the latest news in crypto. Don't forget to download Enkrypt for a seamless web3 multichain wallet experience. Also, if you enjoy using mobile cryptocurrency wallets, give our MEW Mobile app a try, it's available on both iOS and Android platforms!