Many crypto investors spend the majority of their time thinking about what to buy. Which token is undervalued. Which chain is gaining momentum. Which project has the strongest fundamentals. It's a reasonable place to focus — but it's only half the picture.

The other half is how much of each thing you hold. And for most people, that question gets answered by accident rather than intention. You buy what excites you, sell what worries you, and end up with a portfolio shaped more by emotion and market momentum than by any deliberate strategy.

Asset allocation and rebalancing are the tools that change that. They don't require you to predict the market — they require you to have a plan, and then stick to it. Here's what they mean, why they matter, and how they apply specifically to a self-custodial crypto wallet.

This article is for educational purposes only and does not constitute financial advice. All investments carry risk. Always conduct your own research before making any financial decisions.

Jump To:

- What Is Asset Allocation?

- What Each Bucket Does for Your Portfolio

- What Is Portfolio Rebalancing?

- Why Rebalancing Matters More in Crypto

- How to Rebalance in a Self-Custodial Wallet

- Interactive Portfolio Allocation Calculator

What Is Asset Allocation?

Asset allocation is the practice of deliberately dividing your portfolio across different types of assets — not just picking individual assets, but deciding how much weight each category should carry.

The logic behind it is straightforward: different assets behave differently under different market conditions. When one category falls sharply, another may hold steady or even rise. By spreading your holdings across multiple categories, you reduce the risk that any single bad outcome wipes out a significant portion of your portfolio.

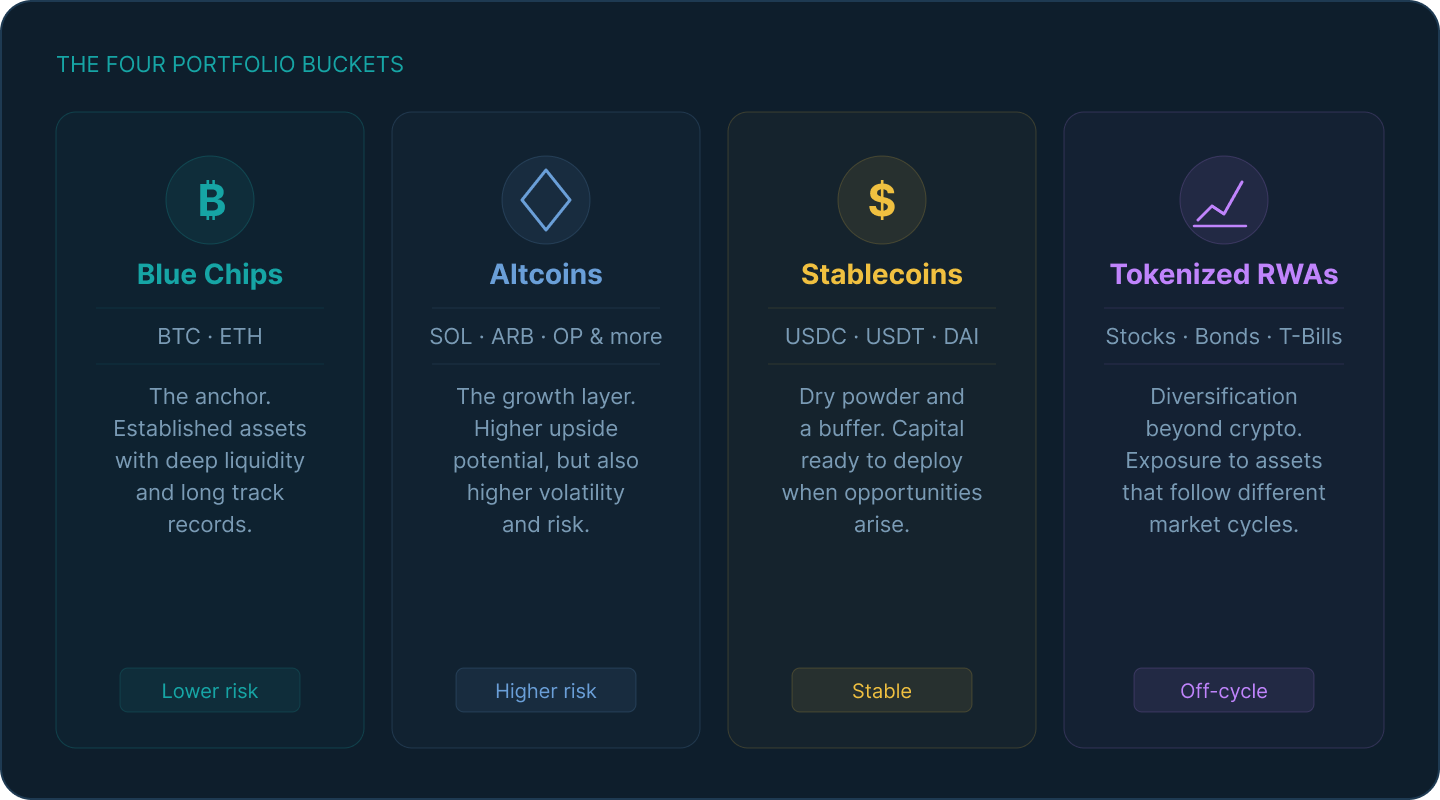

In traditional finance, the classic split is between stocks, bonds, and cash. In a self-custodial crypto wallet, the equivalent buckets look something like this:

- Blue chip crypto — Bitcoin (BTC) and Ethereum (ETH). The most established, most liquid, and generally least volatile assets in the crypto space. The anchor of most crypto portfolios.

- Altcoins and higher-risk assets — Smaller cap tokens, emerging Layer 1s and Layer 2s, DeFi protocols, and other higher-upside, higher-risk assets. The growth layer of your portfolio.

- Stablecoins — USDC, USDT, DAI, and similar assets pegged to the US dollar. They don't grow, but they don't fall either. They act as dry powder — capital ready to deploy when opportunities arise — and as a buffer against crypto market volatility.

- Tokenized real-world assets (RWAs) — Tokenized stocks, treasury bills, and other traditional financial instruments held onchain. These give your portfolio exposure to assets that move independently of crypto market cycles, adding a layer of diversification that purely crypto portfolios lack.

There's no universally correct allocation across these four buckets. It depends on your risk tolerance, your time horizon, and your goals. A conservative long-term holder might weigh heavily toward blue chips and stables. A higher-risk growth-oriented investor might lean into altcoins. What matters is that the split is intentional — not accidental.

What Each Bucket Does for Your Portfolio

Understanding why each category exists helps you make better decisions about how much of each to hold.

Blue Chips — The Anchor

BTC and ETH are the bedrock of most crypto portfolios for good reason. They have the longest track records, the deepest liquidity, the broadest institutional adoption, and the most developed ecosystems. They're still volatile by traditional standards — but relative to the rest of the crypto market, they tend to be more stable and more resilient during downturns.

A meaningful allocation to blue chips gives your portfolio a foundation. When altcoin markets collapse — which they do, regularly — blue chips typically fall less and recover faster. They're not a safe haven in the traditional sense, but they're the closest thing crypto has to one.

Altcoins — The Growth Layer

Higher-risk assets are where the biggest upside in crypto tends to live — and where the biggest losses happen too. A well-chosen altcoin in a bull market can return multiples; a poorly chosen one in a bear market can go to near zero.

The role of altcoins in a portfolio is to provide growth potential beyond what blue chips can offer. But because they carry significantly more risk, the sizing matters enormously. A 5% allocation to an altcoin that drops 80% costs you 4% of your portfolio. A 40% allocation to the same asset costs you 32%. Same asset, very different outcomes — purely because of how much weight it carried.

Stablecoins — Dry Powder and a Buffer

Stablecoins are often underappreciated by investors who see holding cash-equivalent assets as leaving money on the table. In practice, they serve two critical functions.

First, they're dry powder — uninvested capital that can be deployed quickly when the market drops and opportunities appear. Some of the best buying opportunities in crypto history had been available for days or weeks, not months. Investors who were fully invested in other assets had to sell something to buy in; those with stablecoin reserves could act immediately.

Second, they're a buffer. In a highly volatile market, having a meaningful stablecoin allocation reduces the overall swing of your portfolio. A 20% stablecoin allocation means that even if the rest of your portfolio drops 50%, your total drawdown is closer to 40%. The math is simple but the psychological benefit is significant — smaller drawdowns are easier to hold through.

Tokenized RWAs — Diversification Beyond Crypto

Tokenized real-world assets — stocks, government bonds, and other traditional financial instruments represented as on-chain tokens — are the newest addition to the self-custodial investor's toolkit, but they solve an old problem.

Crypto assets are highly correlated with each other. When Bitcoin falls sharply, most of the market falls with it. Stablecoins provide stability, but they don't provide growth. Tokenized RWAs offer something different: exposure to assets that follow different market cycles — corporate earnings, interest rate decisions, macroeconomic trends — rather than crypto-specific sentiment.

For a self-custodial investor, tokenized stocks or tokenized treasuries held in a wallet represent a way to diversify without leaving the onchain ecosystem. Your portfolio can hold exposure to traditional markets and crypto markets simultaneously, from a single wallet.

What Is Portfolio Rebalancing?

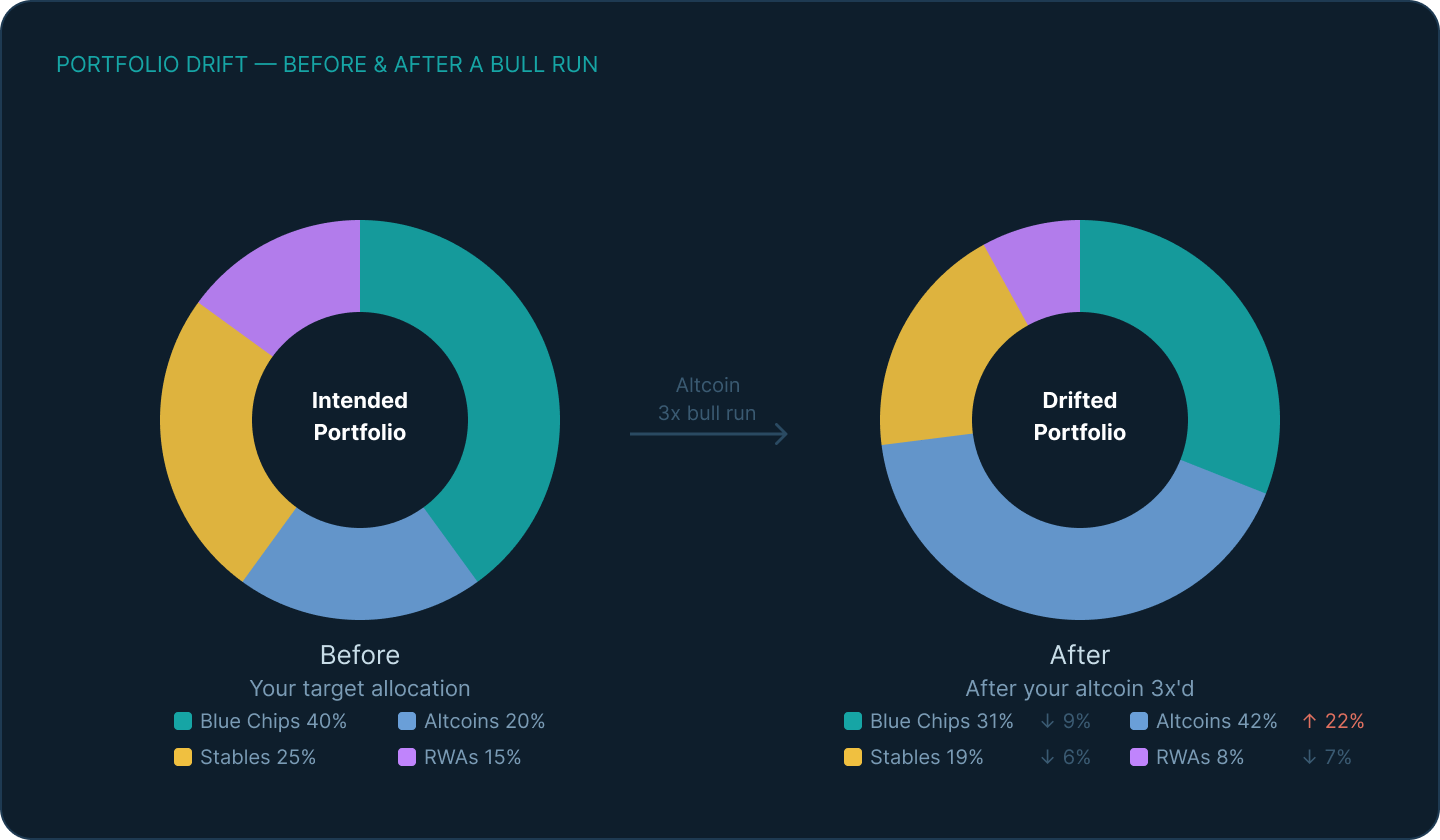

Even if you set a deliberate allocation — say, 40% blue chips, 20% altcoins, 25% stables, 15% RWAs — the market will move those ratios around over time. An altcoin that doubles in value doesn't just make you money; it changes the shape of your portfolio. If it was 20% of your holdings before the move, it might be 35% after. You're now carrying significantly more risk in that asset than you originally intended.

Rebalancing is the process of periodically restoring your portfolio to its target allocation. In practice, this means selling some of what has grown and buying more of what has shrunk — trimming your winners and adding to your laggards.

This runs counter to a natural human instinct. When something is performing well, the temptation is to let it ride. When something is underperforming, the temptation is to avoid it. Rebalancing asks you to do the opposite: take some profit from what's working and redeploy it into what isn't. Done consistently, it enforces a discipline that most investors find nearly impossible to maintain emotionally.

Why Rebalancing Matters More in Crypto

In traditional markets, portfolio drift happens slowly. Equities might outperform bonds over a year, shifting a 60/40 portfolio to something closer to 65/35. That's manageable.

In crypto, drift happens fast. A single altcoin running 3x in a month can transform a balanced portfolio into a dangerously concentrated one almost overnight. The asset you deliberately sized at 10% is now 30% of your portfolio — and if it corrects just as sharply as it ran, that concentration will cost you significantly more than you gained.

Without rebalancing, you're not holding the portfolio you chose. You're holding whatever the market decided for you. The original allocation reflected your risk tolerance and strategy; the drifted one reflects momentum, luck, and timing. Those are not the same thing.

There's also a compounding benefit to rebalancing over time. By systematically trimming assets that have outperformed and adding to those that have underperformed, you're buying relatively low and selling relatively high on a rolling basis — without needing to predict when tops and bottoms will occur.

How to Rebalance in a Self-Custodial Wallet

Rebalancing in a self-custodial wallet is more hands-on than in a managed account, but it's straightforward once you have a process.

Step 1 — Set your target allocation Decide on the percentage you want in each bucket. Write it down. This becomes your benchmark — the portfolio you're always trying to return to.

Step 2 — Track your current allocation regularly Check how your actual holdings compare to your target. Many portfolio tracking tools connect to wallet addresses and give you a real-time breakdown. You're looking for meaningful drift — assets that have moved significantly away from their target weights.

Step 3 — Decide when to rebalance There are two common approaches:

- Time-based rebalancing — Review and rebalance on a fixed schedule: monthly, quarterly, or semi-annually. Simple and consistent, but may trigger rebalancing even when drift is minor.

- Threshold-based rebalancing — Only rebalance when an asset drifts more than a set percentage from its target (e.g. more than 5 percentage points). More efficient, but requires closer monitoring.

Many investors combine both: a regular review schedule, with action only when drift exceeds a threshold.

Step 4 — Execute via swaps In a self-custodial wallet, rebalancing typically happens through swaps — converting an overweight asset directly into an underweight one without leaving your wallet or moving funds to a centralized exchange. This keeps custody with you throughout the process and minimises the steps involved.

Step 5 — Account for fees and tax Every swap has a cost — gas fees, swap fees, and potentially a taxable event depending on your jurisdiction. Factor these into your decisions. Rebalancing too frequently can erode gains through transaction costs. The goal is to keep your allocation broadly on target, not to achieve perfection on every review.

Interactive Portfolio Allocation Calculator

Try out our Interactive Portfolio Allocation Calculator yourself:

Common Mistakes to Avoid

Over-concentrating after a big run An asset that has performed exceptionally well feels safe to hold — it's proven itself. But a large position in any single asset, however strong, creates concentration risk. Trimming winners feels counterintuitive, but it's one of the most important things rebalancing does.

Holding too little in stablecoins Being fully invested sounds optimal — money sitting in stables isn't earning returns. But during market downturns, investors without stablecoin reserves have two choices: hold and watch, or sell something they didn't want to sell to raise capital. Having dry powder costs you some upside; not having it costs you flexibility exactly when flexibility is most valuable.

Ignoring RWAs as a diversification tool Purely crypto portfolios are highly correlated. When sentiment turns negative, most assets fall together. Tokenized RWAs — stocks, treasuries, and other traditional instruments held on-chain — can provide genuine diversification by introducing exposure to different market cycles and drivers.

Rebalancing too frequently Every rebalance has a cost. In crypto, that means gas fees, swap fees, and potential tax events. Rebalancing every week in response to minor fluctuations will eat into your returns faster than you might expect. Set a threshold and stick to it.

Not having a plan in the first place The biggest mistake isn't poor execution — it's having no allocation strategy at all. A portfolio built on impulse buys and emotional sells isn't a portfolio; it's a collection of bets. Having a target allocation, even a simple one, gives you a framework to make decisions against.

Thank you for checking out our Asset Allocation & Portfolio Rebalancing for Self-Custodial Crypto Wallets article! Make sure to follow us on X(Twitter) and let us know your thoughts. Subscribe to our newsletter to stay up to date with MEW releases, and check out our weekly podcast Crypto Currents for the latest news in crypto. For more on the assets covered in this article, check out our guides on stablecoins, tokenized real-world assets, and how to get started with a self-custodial wallet.